Disclaimer: This article is for education only, it is not financial, tax, or legal advice. Investing involves risk, including loss of principal.

In conversations about Investment Trends USA 2026, one pattern keeps showing up again and again, people are not necessarily hunting the “next big thing,” they are rebuilding portfolios to feel steadier.

The common thread is practical comfort, investors want plans they can stick with through rate shifts, inflation worries, and the kind of market swings that make people second-guess everything at 2 a.m.

The author of this guide approaches the topic like an investor-researcher. He tracks retail investor behavior, watches fund-flow data for signs of asset allocation shifts, and reads product documents instead of just headlines.

He also keeps a plain spreadsheet for taxable account optimization and rebalancing rules, because what matters most in 2026 is less about “perfect picks,” and more about repeatable decisions.

How this article helps: It maps where money is moving in the United States across cash tools, bonds, stocks, real assets, alternatives, and crypto, plus how to evaluate each category without hype. It also flags what tends to go wrong, and how people can correct course.

Credibility signals:

- He follows Federal Reserve policy updates and how rate expectations influence portfolios.

- He cross-checks product details using disclosures and filings, and pays attention to the U.S. Securities and Exchange Commission (SEC) framework, along with Financial Industry Regulatory Authority (FINRA) guidance for broker practices.

- He uses “category thinking” similar to Morningstar style comparisons when assessing funds and strategies.

Investment Trends USA 2026: a quick snapshot of what changed

If someone wants the shortest possible summary of what is different now, it is this, risk management became a feature people actively shop for. In prior years, investors talked mostly about returns. In 2026, they talk about “staying invested,” “sleeping at night,” and “not blowing up the plan.”

Risk tolerance recalibration is the real story

The author sees risk tolerance recalibration everywhere, even among experienced investors. It shows up in three common behaviors:

- Higher baseline cash allocations (not forever, but as a shock absorber).

- More structured rebalancing rules, instead of “I’ll do it when it feels right.”

- A tilt toward strategies that feel easier to explain to a spouse, a partner, or a future self.

This is also where volatility management and defensive equity positioning become mainstream vocabulary. Many investors are not trying to eliminate volatility, they are trying to control how it affects their behavior.

Author note: I used to think I had a “high risk tolerance” because I could watch red numbers on a screen and not panic. Then I measured it differently, could I stick with my plan when the market dropped and my life got busy at the same time? That is the real test, and it changed how I size positions and keep cash.

Retail investor behavior looks more systematic now

Another noticeable shift is that investing routines are getting automated. Many people are investing with small amounts monthly and treating it like a bill. That works because it reduces the pressure of timing decisions and supports consistent execution.

This is tightly linked to how to automate investing contributions, which has become a standard feature across major platforms.

In practice, it looks different depending on where someone invests, for example Robinhood emphasizes ease and fractional purchasing, while Charles Schwab and Fidelity Investments tend to offer deeper account tools, research, and tax documents that heavier DIY investors appreciate.

Fees and transparency are getting more attention

A quiet but meaningful trend is active manager fee pressure, partially because investors can now compare costs in seconds. Many people are learning how to compare expense ratios in a way that is not theoretical. They can see, year by year, how fees compound.

A simple process the author uses:

- Compare the expense ratio to the strategy’s complexity (simple index exposure should cost less).

- Check trading spread and liquidity for ETFs, not just the headline fee.

- Look at after-tax behavior if the account is taxable.

He also avoids products that are hard to explain or unusually opaque. In the US, the regulatory system exists for a reason, and investors benefit from understanding the basics of the SEC and FINRA oversight environment.

Where people are putting money first, cash and cash-like tools

High yield cash alternatives became the default “starting line”

In 2026, cash is not just cash. Investors are parking money in high yield cash alternatives while they figure out the rest of their plan, and in many cases they keep a permanent allocation because it reduces the chance of panic selling.

This is where the question where to invest cash safely becomes highly practical. People want yield, but they also want simplicity and quick access.

A useful framing is to split cash into three tiers:

- Bills and near-term obligations.

- Emergency reserves.

- “Opportunity cash,” money that prevents forced selling during volatility.

Cash sweep vs money market funds, what investors actually need to know

A common point of confusion is cash sweep vs money market funds. Sweeps are typically the default cash holding at a brokerage. Money market funds can be a separate product with its own yield, rules, and settlement behavior.

The author watches money market fund inflows because they reflect investor comfort with “earning something while waiting.” When short-term yields are competitive, inflows can rise dramatically, not because investors are bearish, but because they are being more deliberate.

A simple emergency cash ladder that reduces stress

Many investors in 2026 are building a small “cash ladder” for peace of mind, even before they optimize anything else. The emergency fund size rule of thumb varies by household, but the behavioral goal is the same, avoid selling investments during a bad week.

The author separates immediate bills cash from opportunity cash, and he does it for one reason, it prevents forced choices. It is not about maximizing yield, it is about preventing mistakes.

Bonds made a comeback, but people are buying them differently

“Should I buy bonds right now” depends on duration, not headlines

The most common bond question is should I buy bonds right now, and the most useful answer is a framework. The author sees investors moving toward:

- short duration fixed income for stability and rate sensitivity control.

- intermediate term bond allocation when the investor can tolerate more price movement for potentially higher income.

What changed in 2026 is not that bonds became “good” or “bad,” it is that investors learned to match bond duration to their life timeline.

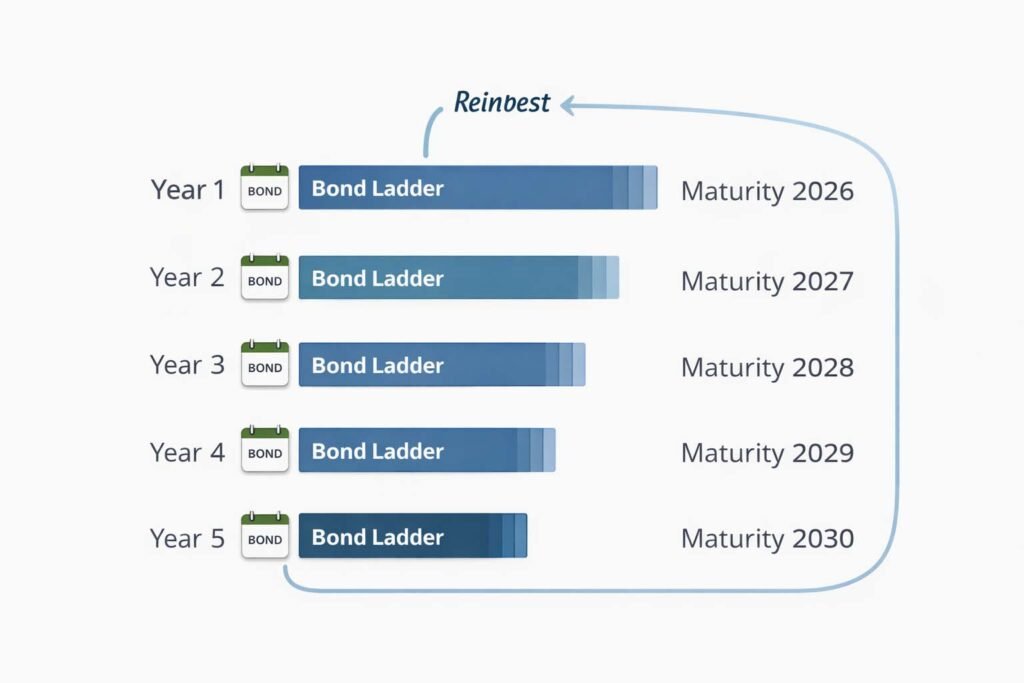

Bond ladder planning, the approach people stick with

When the author sees a bond plan that people actually follow, it is usually bond ladder planning. It reduces timing anxiety and creates a calendar of maturities.

Here is how bond ladders work in plain steps:

- Choose a ladder length (example, 2 to 5 years for short ladders).

- Split the bond allocation into equal rungs (one rung per maturity year).

- As each rung matures, reinvest into the farthest rung to keep the ladder rolling.

- Keep rules written down so reinvestment happens even when markets feel noisy.

Author note: The first time I built a ladder, I made it too complicated. It looked smart on paper and failed in real life. The second time, I used fewer rungs and a simple reinvestment rule, and that one actually stuck.

TreasuryDirect, I Bonds, and inflation protection

For US savers who want direct access to certain government products, TreasuryDirect remains a key doorway. Investors often mention Series I Savings Bonds when inflation is on their minds, and they also use U.S. Treasury Inflation-Protected Securities (TIPS) inside broader bond allocations.

These instruments show up under inflation hedging assets, but the author encourages realistic expectations, they can help with purchasing-power risk, but they are not magic. They need to be sized appropriately and paired with an overall plan.

Credit spread monitoring, a simple risk thermometer

The phrase credit spread monitoring sounds technical, but the idea is simple, when spreads widen, the market is demanding more compensation for credit risk. Many investors use this as a “weather report” for whether they want more Treasuries versus more credit exposure.

This does not require day trading, it is a sanity-check input.

Municipal bond allocation for taxable accounts

For investors with meaningful taxable income and long horizons, municipal bond allocation is often discussed as part of tax efficient investing tips and the broader goal of taxable account optimization.

This is not a blanket recommendation, it is a use-case. The point is that after-tax results matter, and taxes can be a bigger drag than people think.

Stocks are still core, but the “how” is changing

Passive index fund adoption keeps rising

The anchor of many portfolios remains broad stock exposure, but the method is increasingly simple. The author sees strong passive index fund adoption because it is straightforward, diversified, and low cost.

Investors often think in benchmarks, even if they do not buy the index directly. The usual reference points show up constantly, S&P 500, Dow Jones Industrial Average, Russell 2000, plus the large growth narrative associated with Nasdaq.

These indices also connect to the venues where many US equities trade, including the New York Stock Exchange (NYSE) and Nasdaq.

Index funds vs ETFs comparison, what matters in real life

The index funds vs ETFs comparison is not only about cost. It often comes down to:

- Automation (some people like automatic purchases of mutual funds).

- Trading behavior (ETFs can encourage tinkering).

- Tax mechanics and distributions.

- Liquidity, spreads, and transparency.

In provider terms, large issuers dominate mindshare and product design, including Vanguard, BlackRock, iShares, and SPDR (State Street Global Advisors). These names matter because investors care about scale, tracking, and how the fund is managed operationally.

Value vs growth positioning is back on the table

Many investors are revisiting value vs growth positioning, not as a prediction game, but as a way to avoid being unintentionally concentrated.

The author’s approach is to sanity-check valuations using a short list of measures and a common-sense question, “What has to go right for this price to make sense?”

That leads to how to evaluate valuation metrics without drowning in spreadsheets. The author typically focuses on a few consistent measures, compares them to history, and then decides whether to size the position smaller rather than making an all-or-nothing call.

Factor investing strategies are moving from “pro” to mainstream

Another trend is broader adoption of factor investing strategies, not always labeled as “factor” in marketing, but present in portfolio construction.

Two factors the author sees commonly:

- quality factor stocks, companies that tend to have stronger balance sheets and steadier profitability.

- momentum factor exposure, which can work but can also whip around, so it needs guardrails.

Dividend growth screening for “sleep-better” portfolios

Within equity allocation, the author still sees strong interest in dividend growth screening because it aligns with long-term discipline.

It is often tied to dividend investing for steady income, but the author stresses a key nuance, dividends are not guaranteed, and high yield can sometimes signal risk. The goal is quality and sustainability, not just yield.

“Income investing” in 2026, options overlays, covered calls, buffers

Options income overlays, popular and widely misunderstood

The rise of packaged income products is partly about behavior. Investors want cash flow, but they also want a strategy they can hold without constant decision-making. That is where options income overlays show up.

The author’s caution is consistent, these strategies can cap upside, still participate in drawdowns, and create tax complexity, especially in taxable accounts.

Covered call ETF demand, what it is and what it is not

covered call ETF demand has grown because it sounds like a clean trade, “income now.” The reality is outcome-dependent.

Simple scenarios:

- Flat market, covered calls can look attractive.

- Strong bull run, the upside cap can disappoint.

- Sharp sell-off, income does not fully offset the decline.

Buffer ETF popularity, why it feels safer than it is

buffer ETF popularity also reflects a desire to reduce regret. Buffers can soften a defined range of losses over a defined period, but they often come with caps and rules that many investors do not fully internalize.

The author suggests that anyone considering buffer products should summarize the payoff in a single sentence and write down the holding period they intend to follow.

Sector rotation, themes, and the urge to “do something”

Sector rotation signals investors watch

When markets feel uncertain, people seek “signals.” In practice, the author sees investors watching sector rotation signals like shifting rate expectations, earnings leadership changes, and general risk appetite. The problem is that signals are easier to see in hindsight.

This is why defensive positioning, already mentioned earlier, tends to show up here again. Investors often use defensive equity positioning as a “behavioral anchor,” so they do not overtrade.

Thematic ETF flows, the author’s filter for avoiding regret

thematic ETF flows can be driven by storytelling. Themes can work, but they often overlap heavily with broad index exposure, or they concentrate risk in ways investors do not realize until the theme cools off.

The author uses a blunt filter, if the theme’s revenue link cannot be explained in one sentence, it is treated as entertainment, not core allocation. That does not mean “never,” it means “size it like a hobby, not like retirement.”

How to pick sectors to invest in without chasing

For investors asking how to pick sectors to invest in, the author recommends a simple checklist:

- Define the reason (valuation, income, diversification, or a multi-year thesis).

- Set a maximum weight.

- Choose an exit rule (time-based or thesis-based).

- Review the position on a schedule, not during panic.

This is the difference between a plan and a reaction.

Real assets, inflation hedging, and the debate around commodities

Real asset allocation, what it means in practice

In 2026, real asset allocation often includes a mix of REITs, commodities exposure, gold, and inflation-linked bonds like TIPS. Investors are trying to build resilience without making a giant macro bet.

Commodities exposure debate, why it never ends

The commodities exposure debate exists because commodities can behave differently in different regimes. They can help during certain inflationary spikes, and they can also be volatile and frustrating.

The author encourages investors to treat commodities as a diversifier, not as a primary growth engine, and to avoid oversized positions based on short-term narratives.

Gold allocation rationale, when it helps and when it annoys

A common reason people hold gold is psychological, it feels like “insurance.” That is the essence of gold allocation rationale. The author’s view is that gold can play a role as a diversifier, but only if expectations are realistic and the position size is moderate.

REIT portfolio weighting for income and diversification

REIT portfolio weighting remains popular because REITs connect to real-world assets and sometimes provide income. The author emphasizes that REITs are not a uniform category. Different property types can behave very differently, and rate sensitivity can be significant.

Private markets are being “retail-ized”, proceed carefully

Private market access is broader than before

More investors now have some form of private market access, often through packaged vehicles that promise exposure to private equity-like or private debt-like returns. Accessibility is improving, but complexity is also rising.

Private credit demand is the headline, liquidity is the footnote

The author sees rising interest in private credit demand, partly because it is marketed as “income with less volatility.” The fine print matters. Redemption limits, valuation methods, and fee layers can shape real outcomes.

Author note (first-person experience): The most useful habit I learned is to read the liquidity section first. If the product is hard to exit, it should be sized as if it is hard to exit. Many investors do this backwards.

A due diligence checklist the author personally uses

- What are the lockups and redemption gates?

- What fees exist at every layer?

- How is leverage used, if at all?

- What is the manager track record, and what periods does it include?

- What happens in stressed conditions?

This section is not meant to scare people, it is meant to match the product’s risks to its position size.

Crypto in the US investor mix, smaller, more intentional

Coinbase made access easy, but suitability is separate

Crypto ownership has matured into a “satellite allocation” for many investors, and Coinbase is often mentioned because it made access mainstream. That said, ease of buying does not equal suitability for every investor.

Bitcoin and Ethereum as speculative satellite positions

Many portfolios that include crypto focus on Bitcoin and Ethereum, but often at smaller weights and with clearer rules than in prior cycles. The author sees less “all in” behavior and more structured limits.

How to invest more responsibly in high-volatility assets

For anyone looking for how to invest more responsibly in volatile assets, the author’s guidance is consistent:

- Cap the position size.

- Rebalance on a schedule.

- Avoid leverage.

- Keep the “why” written down.

Retirement investing behaviors, boring wins in 2026

Retirement account contribution strategy that people actually follow

A strong retirement account contribution strategy is usually boring, automatic, and designed to survive busy months.

The author’s simplified view of retirement contributions explained is that priorities matter more than perfection. Many US savers start with any employer match, then work outward based on account availability and tax situation.

Target date fund selection remains underrated

target date fund selection remains a practical default for investors who want professional rebalancing and a one-fund approach. The author suggests checking fees, glide path assumptions, and whether the fund matches the investor’s risk tolerance.

Portfolio allocation by age is useful, but not enough

portfolio allocation by age works as a starting point, not as a final answer. The author prefers a three-input model:

- Time horizon.

- Cash needs and job stability.

- Emotional tolerance for drawdowns.

How to invest for retirement if starting late

For readers asking how to invest for retirement, the author emphasizes the basics that work:

- Automate contributions.

- Use broad diversification.

- Keep fees low.

- Avoid strategy hopping.

This links to the best way to build a long term portfolio, which is usually a repeatable system more than a clever pick.

Tax smart moves investors are prioritizing

Tax efficient rebalancing in real life

In taxable accounts, rebalancing can create avoidable tax bills. tax efficient rebalancing often means using new contributions, adjusting inside retirement accounts, and rebalancing with bands instead of constant tinkering.

Tax loss harvesting workflows, done carefully

tax loss harvesting workflows are popular among DIY investors and robo-advisors, but they require awareness of wash sale rules and trading behavior. The goal is to capture losses strategically without accidentally undoing the benefit.

Capital gains harvesting when income is low

capital gains harvesting can be useful for some households in certain income years. The author recommends working with a qualified tax professional if someone wants to do it intentionally, because the details matter.

Taxable account optimization, the silent edge

In 2026, investors are paying more attention to taxable account optimization, including asset location, turnover, and how distributions show up. This is not glamorous, but it can be meaningful.

A practical allocation framework (the section readers bookmark)

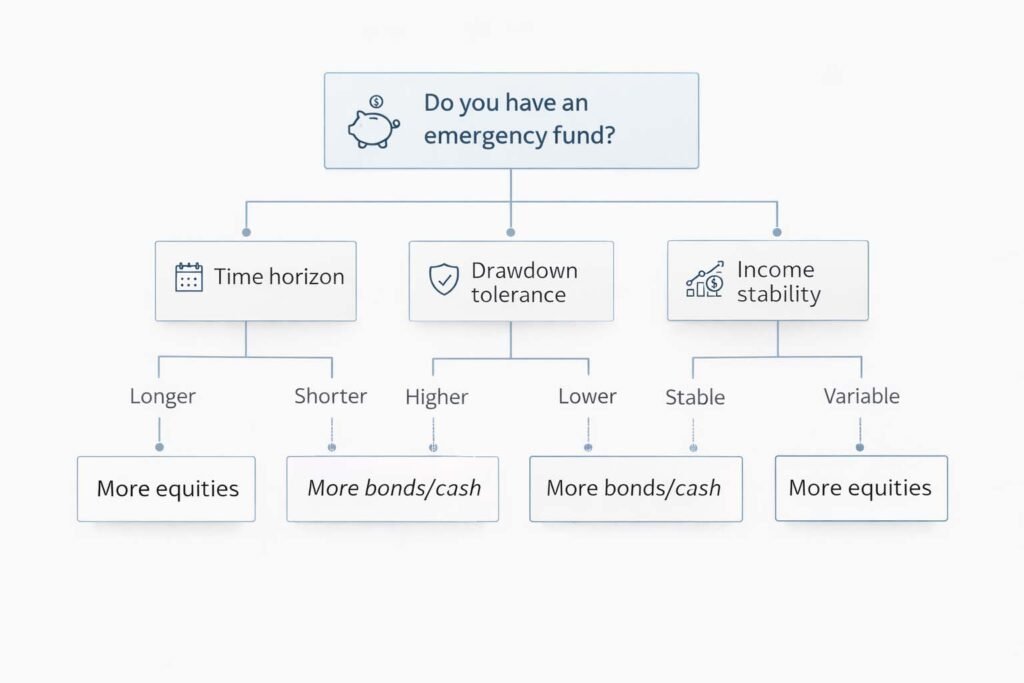

Stocks vs bonds allocation guide, a simple decision tree

A usable stocks vs bonds allocation guide begins with basic questions:

- Is the emergency fund in place?

- What is the time horizon for the goal?

- How painful would a large drawdown feel?

- How stable is household income?

The author suggests writing answers down. People discover that their “risk tolerance” changes depending on which goal they are thinking about.

Diversification strategies that avoid complexity

The most durable diversification strategies are often simple. For readers asking how to diversify without overcomplicating, the author’s core-satellite structure is:

- Core broad equities.

- Core bonds or cash-like allocation.

- Small satellites (factors, REITs, themes, or crypto) with clear size limits.

When to rebalance a portfolio, rules that reduce stress

The question when to rebalance a portfolio is best answered with rules:

- Calendar rebalancing (example, twice a year), or

- Threshold rebalancing (example, when an asset class drifts beyond a band)

The key is to avoid rebalancing based on emotions. This ties back to volatility management, because the real benefit is behavioral consistency.

Dollar cost averaging as behavior management

For readers asking what is dollar cost averaging, it is a systematic approach to investing at regular intervals. It can reduce timing regret and improve consistency, although in certain historical scenarios a lump sum can outperform. The author’s view is practical, the best method is the one someone can stick with through stress.

How to reduce portfolio risk without killing returns

For those searching how to reduce portfolio risk, the author commonly uses:

- Duration management on the bond side.

- A modest quality tilt in equities.

- A cash buffer sized for behavior.

- Position limits to avoid concentration.

Long term vs short term investing, stop mixing buckets

Many mistakes happen when people mix goals. long term vs short term investing becomes much easier when money is bucketed. If money is needed soon, it should not be placed where volatility can force a bad sale.

Picking the tools, brokerages, and products (safely)

Best brokerage for beginners, what the author looks for

When people ask about the best brokerage for beginners, the author’s checklist is practical:

- Clear fee schedule and strong cash management.

- Fractional shares and automation features.

- Reliable tax forms, good support, and solid account protections.

Platform mentions (neutral, non-promotional)

Investors often compare Charles Schwab, Fidelity Investments, Robinhood, and Interactive Brokers depending on their needs. For those who prefer a more hands-off approach, robo-advisors like Betterment and Wealthfront are frequently discussed because they automate deposits and portfolio maintenance.

How to choose an ETF, a simple checklist

For readers searching how to choose an ETF, the author uses:

- Strategy clarity, can it be explained in one sentence?

- Total cost, including spreads and tracking.

- Holdings transparency.

- Provider reputation, such as Vanguard, iShares, SPDR.

This is also where how to lower investing fees becomes practical. Lowering fees is not about chasing the cheapest product blindly, it is about paying only for what truly adds value.

The role of big institutions in product design

Large financial institutions shape product ecosystems, market making, and distribution. Investors hear names like JPMorgan Chase, Goldman Sachs, and Morgan Stanley because these firms participate in building and supporting many parts of modern markets. The author’s view is simple, investors should understand incentives, read disclosures, and choose products based on fit, not brand prestige.

Investing mistakes to avoid in 2026 (based on repeated patterns)

Complexity creep

The author often sees portfolios with too many overlapping funds, theme stacking, and accidental concentration. People can end up with “a lot of funds” but very little real diversification.

Ignoring taxes and fees

Taxes and costs are silent drags. This is why tax planning topics like tax efficient rebalancing and taxable account optimization matter, even though they are not exciting.

Overreacting to headlines

Investors tend to anchor on news, especially when it involves the Federal Reserve. The author encourages a simple rule, if the plan changes every time news changes, there was never a plan.

Not documenting a one-page investment policy

A one-page plan can include:

- Target allocation.

- Rebalancing rule.

- Maximum position size.

- A list of allowed products.

- A short section called “What will not make me change my plan.”

This reduces impulsive decisions and supports long-term execution.

Short 2026 trend map recap, where the money is going

- Cash tools: high yield cash alternatives, money market fund inflows.

- Bonds: short duration fixed income, ladders, municipal bond allocation, TIPS.

- Equities: passive index fund adoption, factor tilts, dividend growth screening.

- Income products: covered call ETF demand, buffer ETF popularity.

- Real assets: REIT portfolio weighting, gold allocation rationale.

- Alternatives: private credit demand, private market access.

- Satellites: Bitcoin and Ethereum.

Before moving to FAQs, one more practical note, the author suggests doing this in order:

- Get the cash plan stable.

- Choose a simple core portfolio.

- Add satellites only after the core works.

That sequence prevents most avoidable regret.

FAQs

1) Where should someone invest cash safely in the US in 2026?

Many investors start with a tiered cash plan, bills cash, emergency reserves, then opportunity cash. The key trade-off is liquidity versus yield. The cash sweep vs money market funds decision often depends on how quickly the money is needed and how the brokerage handles settlement.

2) Should someone buy bonds right now, or wait?

A framework helps more than predictions. If stability matters most, short duration fixed income can reduce rate sensitivity. If the horizon is longer, an intermediate term bond allocation can be considered. Credit spread monitoring can be used as a simple risk check, especially for those reaching for yield.

3) What is the best way to build a long term portfolio without being an expert?

The most repeatable approach is a simple diversified core, often aligned with passive index fund adoption, combined with consistent contributions. Dollar cost averaging can help with behavior, and automation reduces decision fatigue.

4) Index funds vs ETFs, which is better for most people?

The answer depends on behavior and account type. Index funds can support automatic investing, ETFs offer intraday trading and often strong transparency. The index funds vs ETFs comparison should include fees, spreads, and tax considerations, not only the expense ratio.

5) When should someone rebalance a portfolio?

Rules work better than feelings. Threshold bands or a set schedule can support tax efficient rebalancing. In taxable accounts, rebalancing often happens through new contributions to reduce realized gains.

6) How can someone reduce portfolio risk if markets stay volatile?

Diversification strategies plus position limits tend to help. Defensive equity positioning, a cash buffer, and a duration-aware bond allocation are common approaches. The goal of volatility management is not zero volatility, it is avoiding decisions that break the plan.

7) What are covered call ETFs and buffer ETFs, and are they worth it?

Covered call ETFs are built around options income overlays that can generate income but cap upside. Buffer ETFs can soften losses over a defined period but usually include caps and specific outcome windows. Whether they are “worth it” depends on goals, taxes, and holding discipline.

8) Are REITs and gold good inflation hedges?

They can help in some regimes, but they are not perfect substitutes for a full plan. REIT portfolio weighting can add real-asset exposure, while gold allocation rationale often leans on diversification and psychological comfort. The commodities exposure debate exists because results depend heavily on time period and implementation.

9) What does tax loss harvesting mean, and when does it matter?

Tax loss harvesting workflows aim to realize losses to offset gains, but they require careful attention to wash sale rules. It matters most in taxable accounts and for investors with meaningful realized gains or ongoing tax planning.

10) How much crypto is reasonable for a typical portfolio?

Many investors treat it as a small satellite position, if they use it at all. Coinbase makes access easy, but Bitcoin and Ethereum are still volatile. A responsible approach uses strict sizing caps, scheduled rebalancing, and no leverage.

Author Bio

Evan Caldwell writes about personal finance and investing with a focus on practical, evidence-based decision making for everyday investors. He covers portfolio construction, risk management, and tax-aware investing in plain English. Published by Ahmed Saeed.